ALL 50 US STATES + US FEDERAL + CANADA COVERAGE

US and Canada Regulatory Compliance Platform

FinregE monitors federal and state regulatory requirements across all 50 US states and Canada, managing overlapping obligations between SEC, FINRA, OCC, CFPB, NYDFS, OSFI, CSA, US state banking departments, and 25+ state privacy laws in one platform, at obligation level.

FinregE won contract to create, host, maintain and manage the FCA Handbook

Strategic investment by Moody’s

Active clients across North America of all sizes

Measured outcomes across our client base

2,000+

regulatory sources monitored across federal and state across the US & Canada

160+

countries covered, North America is fully integrated into FinregE's global regulatory intelligence infrastructure

95%

reduction in manual compliance workload reported by FinregE clients

24-hour SLA

from source publication to platform availability including federal and state sources

95%+

reduction in manual compliance workload reported by FinregE clients

4-12 weeks

from implementation to measurable return on investment

Every North American financial regulator. 24/7 monitoring. AI RIG interpretation on every publication.

FinregE monitors all US and Canadian financial regulators, capturing rules, guidance, no-action letters, examination findings, enforcement actions, speeches, and regulatory priorities across the SEC, FINRA, OCC, CFPB, CFTC, FinCEN, CSA, OFSI and more.

AI RIG interprets every publication and extracts specific obligations for each firm type, capturing every overlap to prevent duplicative efforts.

Key challenges faced by North American firms

Diverging definitions

The same term means different things in different states. Deadlines, exemptions, and enforcement vary wildly.

What actually applies?

Working out what applies, what changed, and what differs across jurisdictions consumes hours of manual effort.

Proving implementation

Tracking who needs to act, which policy is affected, and how to prove the change was implemented.

Timing & coordination

Multiple states publish similar rules at different times, creating duplicate work and missed connections.

AI RIG: Your AI expert for Canada and US state & federal regulations

AI RIG gives firms a faster, more controlled way to operationalise regulatory change.

It helps compliance teams understand new requirements, identify what matters, and assess impact with greater speed and consistency, while giving senior management clearer visibility of implementation, ownership, and risk.

Built specifically for regulatory use cases, AI RIG supports explainable, auditable decision-making in environments where trust, traceability, and control matter as much as efficiency.

How we make US & Canadian regulatory compliance easy

US regulatory compliance is difficult because teams must interpret 50-state differences, understand federal overlap, coordinate action across the business, and prove implementation later. FinregE is built to connect those steps in one end-to-end infrastructure.

In Canada, financial services firms must comply with multiple regulators, requiring coordination across federal, provincial, and self-regulatory bodies, as well as clear alignment of obligations, implementation, and reporting. FinregE brings the same end-to-end structure to this fragmented landscape, enabling firms to manage regulatory change, execution, and evidence in a single system.

Real-time monitoring

All 50 states and federal bodies covered. All Canadian regulators covered.

AI deduplication

Cut duplicate alerts and repeated effort.

Smart filtering

See what is relevant to your business.

Cross US state comparison

Understand where states diverge.

Plain English translation

Turn legal text into practical understanding.

Policy, risk & control mapping

Connect regulation to your internal framework.

Workflow and ownership

Make action clear across the business.

Audit-ready evidence

Prove what changed and what was done.

Automated end-to-end regulatory compliance for US and Canada

FinregE has active clients in North American financial services. The platform covers federal and state regulation across banking, insurance, asset management, payments, and fintech, for firms of every size. We also cover other regulated sectors such as energy, automotive, health, HR and more.

The complete compliance operating layer for US and Canadian financial services

The AI-native infrastructure behind every North American jurisdiction

US and Canadian regulation is shaped by overlapping authorities and constant legislative and supervisory change, whether through federal and state divergence in the US or a multi-layered system of federal, provincial, and self-regulatory bodies in Canada. FinregE helps firms manage this complexity with connected regulatory intelligence, AI-assisted analysis, internal mapping, and audit-ready workflows.

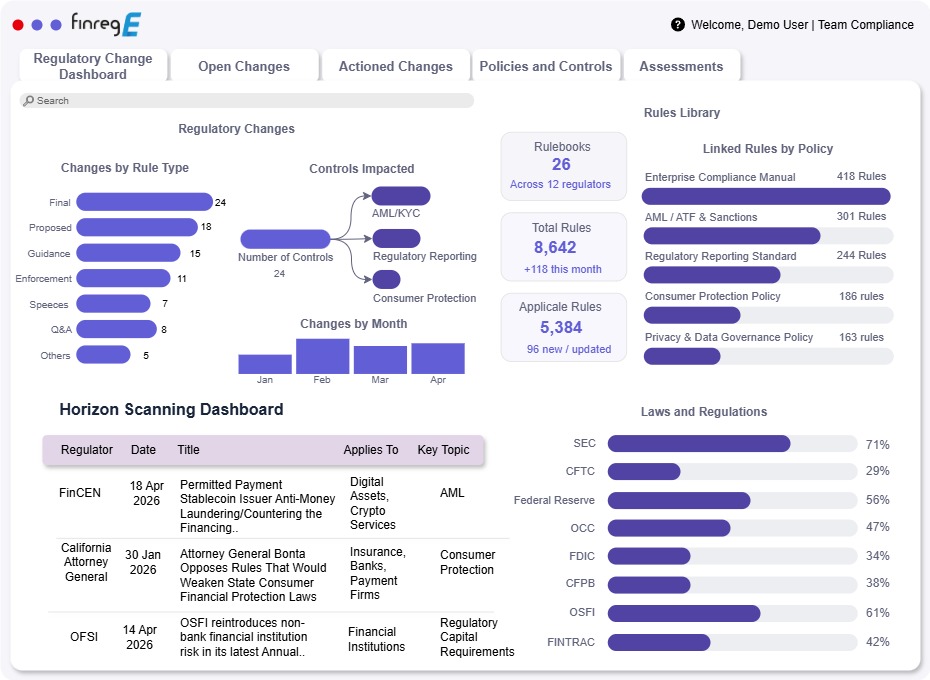

Comprehensive North America horizon scanning in one feed

We help firms stay ahead of state and federal regulatory change with broad, structured coverage across the US, Canada and beyond. Regulatory updates are captured within 24 hours of publication, interpreted by AI RIG, structured into a plain-English briefing note showing what changed, what it means, who it applies to, and what action is required.

We monitor all 50 US states alongside 160+ countries, capturing new laws, proposals, consultations, enforcement actions, and supervisory developments in one place. This gives firms a stronger foundation for identifying what matters early and managing cross-border compliance with greater consistency.

Regulatory Obligations that manage overlaps and differences

AI RIG extracts obligations from every applicable federal and state regulatory framework and manages the overlap. For example, when NYDFS cybersecurity requirements exceed SEC requirements in specific areas, AI RIG identifies the combined obligation. When state consumer protection law is more stringent than CFPB UDAAP in a given state, AI RIG flags it. The obligation inventory reflects the real compliance requirement; the most stringent applicable standard across the full federal and state framework.

Digital Rulebooks, your regulatory footprint structured

A Digital Rulebook built to the firm’s exact regulatory footprint, consisting of federal regulators, states of operation, and Canadian rulemakers. Every rule in every applicable jurisdiction, structured consistently, searchable, and connected to AI RIG for instant interpretation. For firms with multi-state footprints, the Digital Rulebook replaces the combination of regulator website bookmarks, PDF libraries, and institutional memory that currently passes for regulatory knowledge management.

Policies, controls and evidence built in

FinregE helps firms connect regulatory change to the internal frameworks that matter most: policies, risks, controls, standards, and testing.

Rather than stopping at identification, the platform helps compliance teams understand where change lands internally, what needs to be updated, and how that response will be evidenced. The result is a more joined-up, defensible approach to regulatory implementation.

AI RIG MAPS: gap analysis across the combined federal and state obligation set

AI RIG MAPS maps the combined federal and state obligation set against internal policies, procedures, and controls, simultaneously, in seconds. A gap analysis that previously required separate consultant engagements for each jurisdiction now runs across the full multi-state or multi-regulator obligation inventory at once. Partial coverage, where the policy addresses the federal obligation but not the more stringent state requirement, is identified with specific language to close each gap.

AI RIG for obligation-level regulatory compliance

For North American firms, AI RIG provides the structured obligation inventory and documented compliance programme analysis of every law, rule or regulatory change. Every obligation identified. Every coverage gap assessed. Every assessment documented.

Proven with regulators. Trusted by regulated institutions.

FinregE’s regulatory data and AI capabilities are trusted by major financial institutions, government bodies, and regulators that need to manage complex obligations across jurisdictions with greater structure, traceability, and scale.

UK FCA Handbook

Selected by the UK Financial Conduct Authority through a competitive process to redesign, host, and manage the FCA Handbook, helping make regulation easier to navigate, compare, and apply.

Moody's investment

Backed by Moody’s Corporation, one of the world’s leading financial data and analytics organisations, reinforcing FinregE’s long-term credibility and strategic relevance.

Global partnerships

FinregE collaborates with leading regulators and organisations across sectors to innovate and solve real-world regulatory challenges.

Every financial regulator. Every publication type. Every obligation extracted.

FinregE monitors all major US federal financial regulators and Canadian regulators, capturing rules, guidance, no-action letters, examination findings, enforcement actions, speeches, and regulatory priorities, with AI RIG interpreting every publication and extracting the specific obligations it creates for each firm type.

Regulator | Full name | Primary compliance areas monitored by FinregE |

|---|---|---|

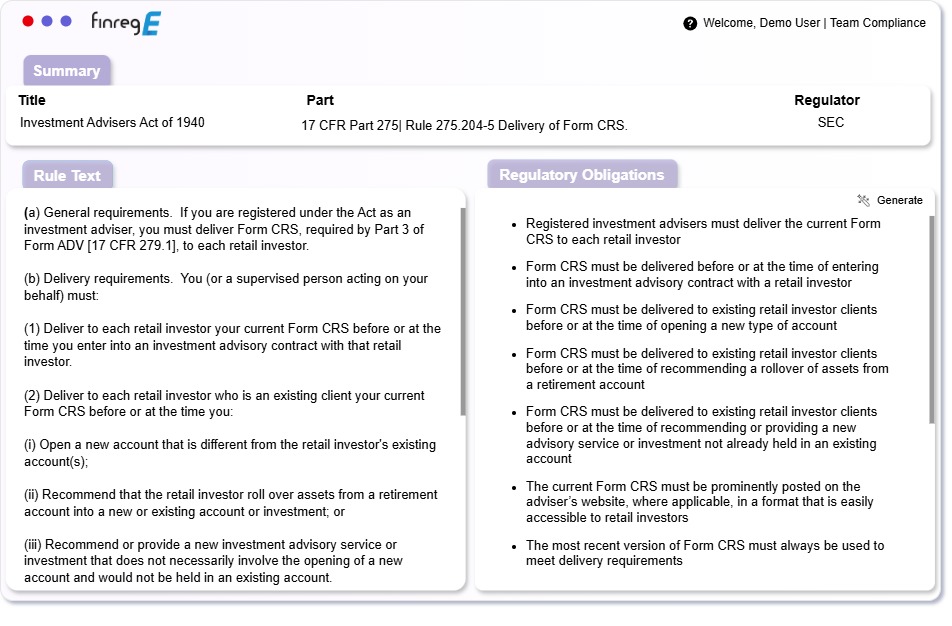

SEC | Securities and Exchange Commission | Investment advisers, broker-dealers, investment companies, public companies — Rule 206(4)-7 compliance programmes, Regulation Best Interest, Form CRS, cybersecurity disclosure rules, climate disclosure requirements |

FINRA | Financial Industry Regulatory Authority | Broker-dealer supervision (Rule 3110), suitability and best interest, AML programme requirements, continuing education, product approvals |

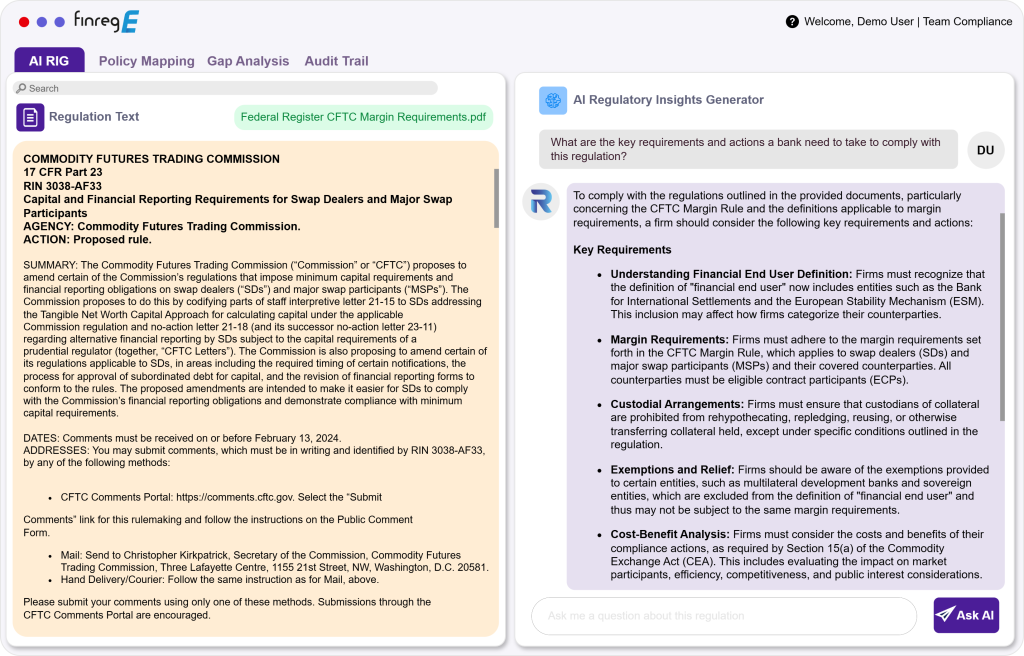

CFTC | Commodity Futures Trading Commission | Swap dealers, commodity pool operators, commodity trading advisers, swap margin rules, reporting obligations, business conduct standards |

OCC | Office of the Comptroller of the Currency | Nationally chartered banks and federal savings associations. Heightened Standards, credit risk, operational risk, compliance management systems |

Federal Reserve | Board of Governors | Bank holding companies, systemically important institutions, foreign banking organizations, capital requirements, stress testing, resolution planning. |

CFPB | Consumer Financial Protection Bureau | Consumer financial products; TILA, RESPA, ECOA, FCRA, HMDA, UDAAP, mortgage servicing, debt collection rules |

FDIC | Federal Deposit Insurance Corporation | State non-member banks — deposit insurance, safety and soundness, consumer protection, resolution authority |

FinCEN | Financial Crimes Enforcement Network | BSA/AML programme requirements, beneficial ownership reporting (CTA), suspicious activity reports, currency transaction reports |

NCUA | National Credit Union Administration | Federal credit unions — share insurance, capital requirements, consumer protection, cybersecurity guidance |

HUD/FHA | Housing and Urban Development | Mortgage lenders and servicers — FHA programme requirements, fair housing obligations, servicing standards |

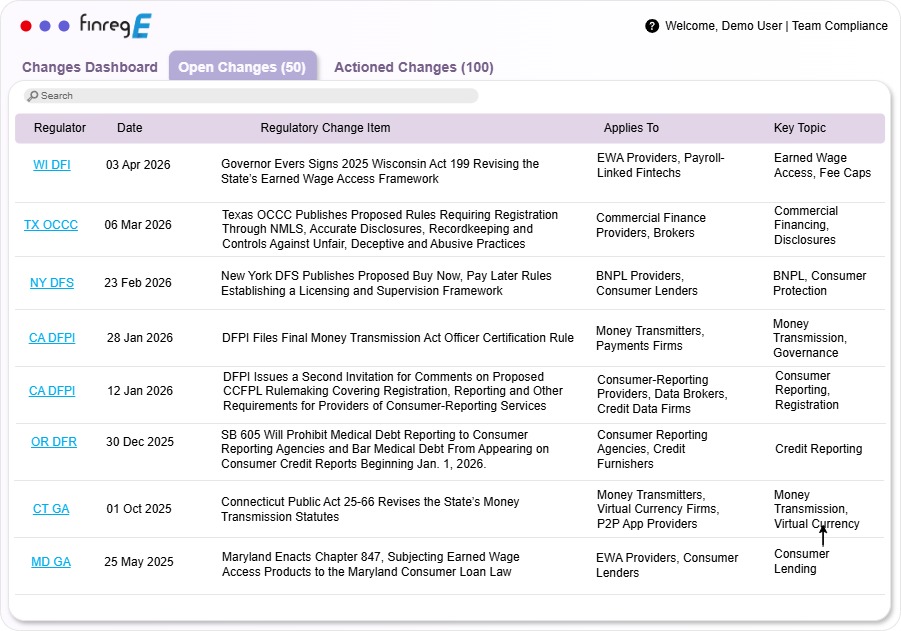

All 50 states. Every state financial regulatory authority. The monitoring infrastructure that did not previously exist.

FinregE monitors every type of state financial regulatory authority across all 50 states, banking departments, insurance departments, securities regulators, attorney general consumer protection offices, state legislatures, and state fintech and digital asset regulatory bodies, with the same automated intelligence infrastructure it applies to federal regulation.

State regulatory area | Key authorities | What FinregE monitors |

|---|---|---|

State banking regulation | 50 state banking departments | State-chartered bank examination requirements, state lending laws, state consumer protection regulations — each state with its own examination cycle and regulatory priorities |

New York DFS | Department of Financial Services | 23 NYCRR 500 cybersecurity regulation, virtual currency regulation (BitLicense), New York Banking Law, consumer financial protection, insurance regulation |

California DFPI | Dept of Financial Protection and Innovation | California Consumer Financial Protection Law, California Financing Law, Money Transmission Act, CCPA/CPRA financial services implications |

State insurance regulation | 50 state insurance departments | NAIC model regulations adopted at state level — rate filings, form approvals, solvency requirements, market conduct examinations differ by state |

State securities regulation | 50 state securities regulators (NASAA) | Blue Sky laws, state investment adviser registration thresholds, state broker-dealer requirements, state money transmitter requirements |

State privacy laws | 25+ state comprehensive privacy laws | California CCPA/CPRA, Virginia VCDPA, Colorado CPA, Connecticut CTDPA, Texas TDPSA, Montana, Oregon, and 20+ more — each with different scope, rights, and financial services carve-outs |

State AML and financial crimes | 50 state AGs, banking departments | State money transmission laws, state-level AML requirements beyond federal BSA, state unclaimed property laws, consumer lending usury limits |

State mortgage regulation | NMLS states, state banking departments | State mortgage licensing, state foreclosure requirements, state predatory lending laws, state servicing standards — critical for non-bank mortgage companies |

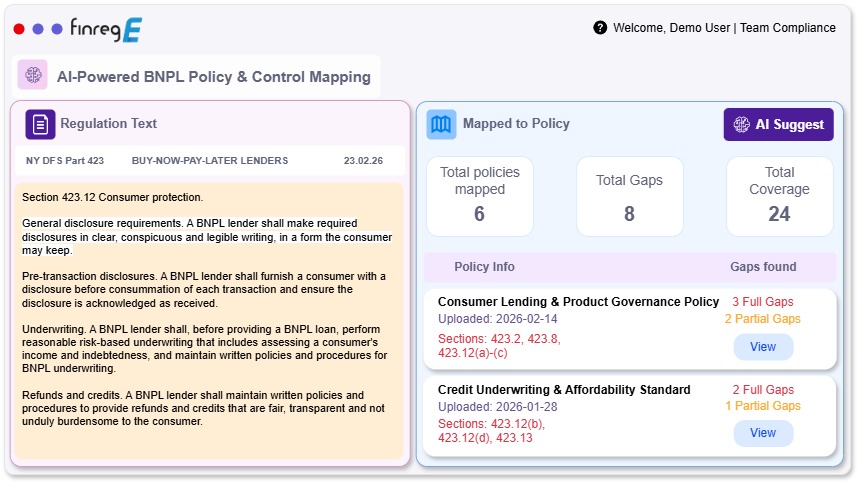

State fintech and digital assets | Emerging state frameworks | Arizona, Utah, Wyoming, Texas fintech sandboxes; state crypto regulation; earned wage access; buy now pay later state frameworks |

ALL 50 STATES

State regulatory monitoring

For every firm size

For large financial institutions, FinregE consolidates 50-state regulatory monitoring into one platform, eliminating the dedicated team and consultant spend currently required to maintain this coverage.

For mid-size regional firms operating across 5 to 20 states, FinregE provides the monitoring infrastructure that previously only large firms could afford.

For community banks, credit unions, state-chartered entities, fintechs with MTL portfolios, and state-registered investment advisers, FinregE makes comprehensive state regulatory compliance achievable for the first time, at a scale appropriate to smaller compliance teams.

Federal and state requirements do not exist in parallel. They overlap. FinregE manages the intersection.

Most regulatory compliance requirements involve at least three layers simultaneously; federal minimums, state requirements in each state of operation, and the intersection between them where state law exceeds, modifies, or conflicts with federal standards.

A bank subject to NYDFS 23 NYCRR 500 must also meet SEC cybersecurity rules, FTC Safeguards requirements, and up to 50 different state data breach notification laws, each with different timelines, thresholds, and recipient lists.

AI RIG identifies these overlaps automatically, extracting requirements from each applicable framework, comparing them obligation by obligation, and identifying where the most stringent standard applies. RIG MAPS maps the combined obligation set against internal policies, identifying gaps in the combined coverage, not just single-framework coverage.

Regulatory area | Overlapping requirements | How FinregE manages the overlap |

|---|---|---|

Cybersecurity | NYDFS 23 NYCRR 500 + SEC cyber rules + FTC Safeguards + state data breach notification laws (50 different thresholds and timelines) | AI RIG identifies overlapping requirements across all applicable frameworks, extracts the most stringent standard in each area, and flags where state requirements exceed federal minimums |

Data privacy | CCPA/CPRA + VCDPA + CPA + 20+ state privacy laws + GLBA financial privacy + SEC data protection rules | RIG MAPS identifies which state privacy obligations apply to each entity and business line, maps them against the firm’s privacy notices and procedures, and identifies gaps across the combined state and federal framework |

AML / BSA | FinCEN BSA programme + state money transmission AML requirements + NYDFS transaction monitoring requirements + FINRA AML obligations | FinregE tracks all applicable AML obligations simultaneously, identifies where state requirements exceed BSA minimum standards, and maintains a combined obligation inventory across all applicable jurisdictions |

Consumer protection | CFPB UDAAP + state UDAP laws (50 variations) + state consumer lending laws + state debt collection laws | AI RIG extracts the specific state-level consumer protection obligations applicable to each business line, compares them against federal standards, and identifies the most stringent requirement applicable in each state |

Mortgage / lending | TILA + RESPA + HMDA + state mortgage licensing + state predatory lending laws + state servicing requirements | FinregE monitors federal and state mortgage regulation simultaneously, tracks state licensing requirements across all NMLS-participating states, and alerts when state requirements differ materially from federal standards |

Crypto / digital assets | SEC crypto guidance + CFTC jurisdiction + FinCEN money transmission + NYDFS BitLicense + state money transmission laws (40+ state MTL requirements) | FinregE tracks the rapidly evolving federal and state crypto regulatory framework, monitors state MTL requirement changes across all 50 states, and maps overlapping obligations for firms operating across multiple jurisdictions |

End-to-end regulatory compliance for Canada

Canada’s financial regulatory framework combines federal prudential regulation (OSFI), federal financial crimes regulation (FINTRAC), and a complex provincial system, with Quebec operating under a distinct civil law framework and the most stringent privacy requirements in North America. FinregE covers the full Canadian regulatory landscape.

Regulator | Full name / scope | Primary compliance areas monitored by FinregE |

|---|---|---|

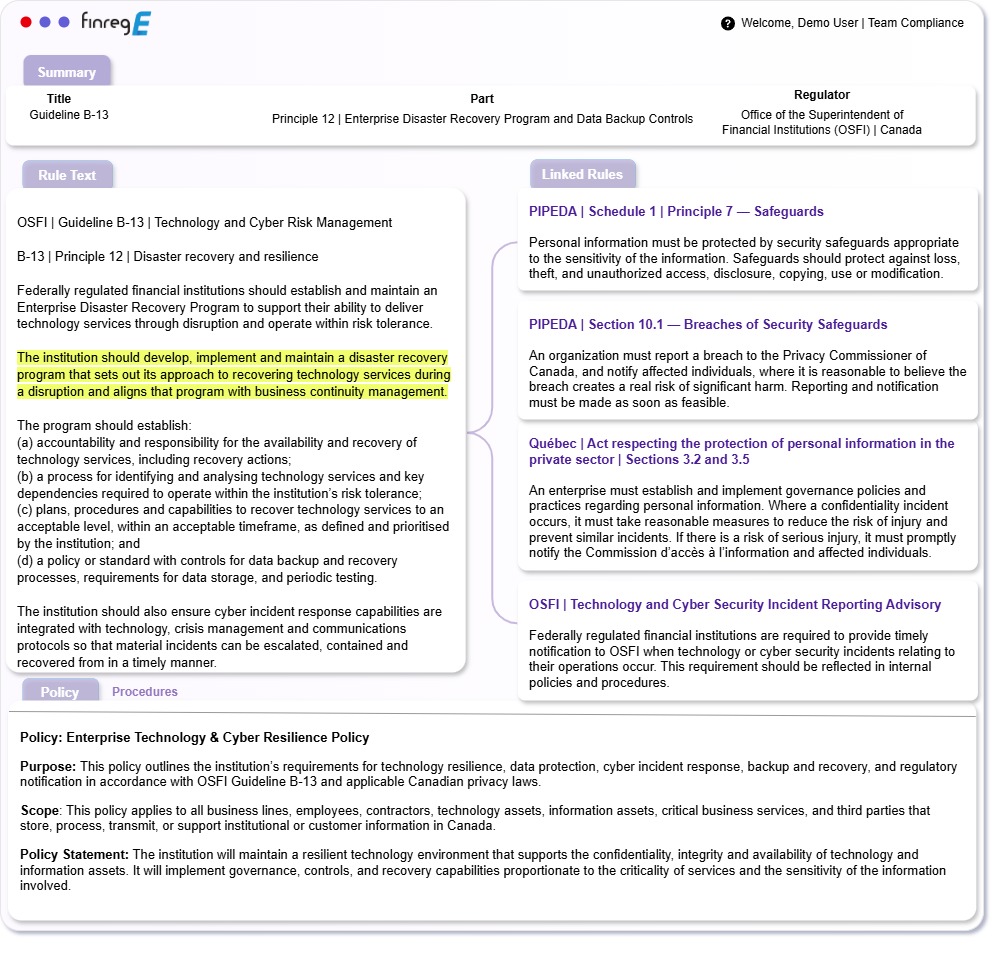

OSFI | Office of the Superintendent of Financial Institutions | Federal prudential regulation — capital, liquidity, operational resilience, B-20 mortgage underwriting guidelines |

FINTRAC | Financial Transactions and Reports Analysis Centre | AML and ATF obligations — Proceeds of Crime Act, beneficial ownership reporting, STR and CTR requirements |

CIRO | Canadian Investment Regulatory Organization | Investment dealers and mutual fund dealers — conduct, registration, product suitability, market integrity |

OSC | Ontario Securities Commission | Provincial securities regulation — registration, prospectus, continuous disclosure, derivatives |

AMF | Autorité des marchés financiers (Quebec) | Quebec financial sector regulation — financial institutions, securities, insurance, and derivatives |

BCSC | BC Securities Commission | Provincial securities regulation for British Columbia — registration, enforcement, exempt market dealers |

PIPEDA / Law 25 | Federal and Quebec privacy law | Federal privacy law (PIPEDA) and Quebec Law 25 — among the most stringent privacy obligations in North America for firms with Quebec operations |

Quebec: the compliance layer most US firms miss

Quebec’s Law 25, significantly strengthened in recent years, now creates privacy obligations for financial services firms with Quebec operations that exceed both PIPEDA and most US state privacy laws. FinregE monitors Quebec regulatory developments in French at source, with AI RIG producing English-language obligation extracts. For US firms with Canadian operations, Quebec is the compliance layer most commonly under-monitored, but not by us.

Three states that consistently define what the rest follow

New York Department of Financial Services

NYDFS' regulatory output regularly sets national standards that federal agencies subsequently adopt. 23 NYCRR 500, the cybersecurity regulation, created obligations that the SEC and FTC have since paralleled at the federal level. The BitLicense virtual currency framework remains the most developed state crypto regime in the country. NYDFS climate financial risk guidelines preceded federal action. FinregE monitors all NYDFS publications and maps the NYDFS requirements against overlapping federal standards for every firm.

California DFPI and the California regulatory ecosystem

California has built the most comprehensive state consumer financial protection framework in the country. The CCPA/CPRA adds significant privacy obligations for financial services firms on top of GLBA, with a complex set of financial services exemptions that vary by obligation type. FinregE monitors the DFPI, California legislative activity, and the CCPA/CPRA privacy framework, tracking how California consumer protection, financing law, money transmission, and privacy requirements interact with federal standards and with each other.

State privacy law patchwork, 25+ states

The United States has 25+ state comprehensive privacy laws, each with different scope, rights, exemptions, and compliance timelines. For financial services firms, the interaction between state privacy laws and GLBA is particularly complex. FinregE tracks every state privacy law as it passes, is amended, and takes effect, extracting the obligations applicable to firms, mapping the GLBA exemption scope in each state, and identifying where state obligations apply.

FINREGE FOR EVERY SIZE OF REGULATED FIRM

Built for national institutions. Scaled for community banks, credit unions, and fintechs

Large financial institutions

We consolidate federal and multi-state regulatory monitoring into one platform, eliminating the separate monitoring streams for each federal and state regulator. RIG MAPS provides obligation-level gap analysis , running automatically as regulations and internal documents change.

Regional and community banks

FinregE covers the full federal and state regulatory footprint automatically, pre-interprets every update through AI RIG, and routes relevant changes into structured impact assessments. The compliance team gets back the capacity to respond to regulatory change rather than just find it.

Credit unions

NCUA federal oversight or state credit union regulator oversight, CFPB requirements, FinCEN BSA obligations, and state-level consumer and privacy requirements, FinregE provides credit unions with the same automated regulatory intelligence available to larger institutions, at a scale appropriate to a member-focused financial cooperative.

State-registered investment advisers

Automate compliance workflows across consumer credit, affordability, interest rate risk, and fair lending rules. Track changes in FCA, CFPB, SEC and prudential frameworks, linking them directly to credit policies and control procedures.

Why federal-only regulatory monitoring leaves every firm with gaps

The largest financial institutions have built dedicated state regulatory affairs teams and spend significantly on consultant relationships to manage multi-state regulatory footprints. They have the resources to track 50 state banking departments, 50 state insurance regulators, 50 state securities regulators, and the growing patchwork of state privacy, fintech, and consumer protection laws.

Most firms do not. The state regulatory landscape is also accelerating; 25 states have passed comprehensive privacy laws in the last three years, New York DFS has issued major new cybersecurity and crypto requirements, California has significantly expanded its consumer financial protection regime, and states are legislating ahead of federal action on AI, digital assets, and earned wage access.

Most regulatory compliance platforms monitor the federal layer. They capture the federal rule. They may capture some examination guidance. They rarely capture the state banking department examinations, the state insurance commissioner bulletins, the state securities regulatory notices, or the attorney general consumer protection opinions that contain the operational compliance detail for firms doing business in those states.

FinregE monitors the full stack. Federal first. Then every state. Then the overlaps between them. That is the compliance infrastructure North American financial services has been waiting for.

We’re here to answer all your questions

FinregE specialises in providing standard and bespoke regulatory compliance modules to help deliver automation, speed and efficiencies in managing regulatory compliance processes.

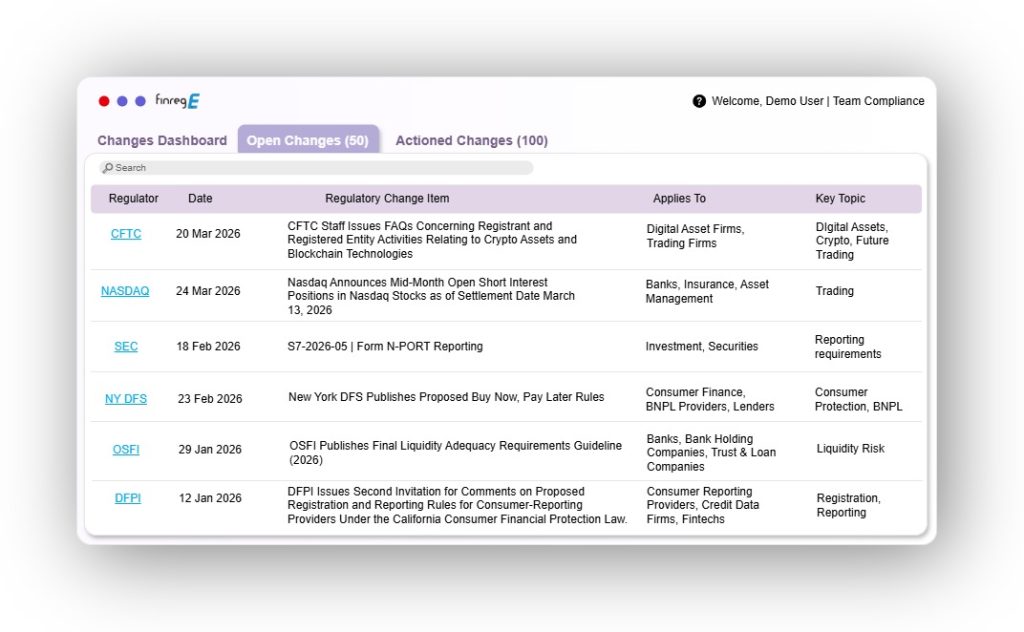

Does FinregE monitor US state regulatory requirements, not just federal?

Yes. FinregE monitors regulatory requirements across all 50 US states and Canada — covering state banking departments, state insurance regulators, state securities regulators, state attorneys general consumer protection offices, state privacy regulators, state money transmission regulators, and state legislatures. This includes the New York DFS, California DFPI, and every other state financial regulatory authority. FinregE is one of the few regulatory compliance platforms to provide comprehensive state-level monitoring alongside federal regulatory coverage.

How does FinregE manage overlapping federal and state regulatory requirements?

AI RIG extracts obligations from every applicable federal and state regulatory framework and identifies where they overlap, diverge, or conflict. For each area of overlap, AI RIG identifies which standard is most stringent and what the combined compliance obligation is. RIG MAPS then maps the combined obligation set against internal policies and controls — identifying gaps in the combined coverage, not just any single regulatory framework. A firm operating under NYDFS 23 NYCRR 500, SEC cybersecurity disclosure rules, and the FTC Safeguards Rule simultaneously gets a single, integrated compliance view rather than three separate analyses.

Can FinregE help community banks and credit unions manage state and federal compliance?

Yes. FinregE scales to smaller compliance teams — providing the same automated regulatory intelligence to community banks and credit unions that large institutions use. A community bank operating in three states gets federal regulatory monitoring alongside all three state banking department feeds, state consumer protection requirements, and state privacy law developments — pre-interpreted by AI RIG and routed into structured workflows. This is the monitoring capability that previously required consultant relationships most community banks cannot afford.

Does FinregE cover state privacy law compliance for financial services firms?

Yes. FinregE monitors all 25+ state comprehensive privacy laws — including California CCPA/CPRA, Virginia VCDPA, Colorado CPA, Connecticut CTDPA, Texas TDPSA, and all subsequent state privacy legislation — alongside federal GLBA. For financial services firms, FinregE maps the GLBA exemption scope in each state, identifies where state obligations apply despite the exemption, and extracts the specific obligations applicable to each state of operation.

Does FinregE cover Canadian financial regulatory requirements?

Yes. FinregE monitors the full Canadian federal and provincial financial regulatory framework — OSFI prudential requirements, FINTRAC AML and ATF obligations, CIRO investment dealer requirements, and provincial securities regulators including the Ontario Securities Commission, Autorité des marchés financiers (Quebec), and British Columbia Securities Commission. Quebec’s Law 25 privacy requirements are monitored in French at source with English-language obligation extracts produced by AI RIG.

How does FinregE's software help with regulatory compliance?

FinregE’s software helps with regulatory compliance by providing a centralized repository for all your regulatory requirements, policies, and processes. It also helps you identify any gaps against the requirements and any regulatory changes on the horizon against the rule and requirements, ensuring that you remain fully compliant with all relevant regulations.

How does FinregE cover NYDFS 23 NYCRR 500 cybersecurity requirements?

FinregE monitors all NYDFS regulatory publications including the cybersecurity regulation and its amendments — extracting the specific obligations applicable to covered entities and mapping NYDFS requirements against federal SEC and FTC cybersecurity standards to identify the combined compliance obligation for firms subject to multiple frameworks. For firms navigating the overlap between NYDFS 500, SEC cybersecurity disclosure rules, and the FTC Safeguards Rule, FinregE produces the integrated obligation view that each framework in isolation does not.

Does FinregE help with SEC Rule 206(4)-7 compliance programme requirements?

Yes. SEC Rule 206(4)-7 requires registered investment advisers to adopt policies and procedures reasonably designed to prevent violations — which the SEC interprets as requiring firms to identify their specific obligations and demonstrate that their compliance programme addresses each one. FinregE provides the structured obligation inventory that the SEC’s Division of Examinations looks for — every applicable obligation extracted by AI RIG, every coverage gap identified by RIG MAPS, every assessment documented in the audit trail. The compliance programme the examiner evaluates is a programme where reasonable steps are visible, evidenced, and complete.

The full US regulatory stack. Every state. Canada. One platform.

Federal compliance is not the full picture for any firm with state operations. State compliance is not achievable at scale without automated infrastructure. The intersection between federal and state requirements is where compliance gaps and enforcement actions live — and where no previous platform has operated at the obligation level.

FinregE covers all of it. Today.