Publication Date: 2024-03-19 | Regulator: UK FCA

Title: FCA Business Plan 2024/25

Summary

The document outlines the key activities and commitments of the Financial Conduct Authority (FCA) for the year 2024/25. The FCA aims to ensure competition in the interests of consumers, maintain appropriate access to financial services, and support consumers in managing their debts sustainably.

Key activities for 2024/25 include encouraging innovation and evolving markets, updating the regulatory framework, delivering primary market policy reforms, consulting on regulatory changes for investment research payment options, and ensuring venues and derivative markets are resilient.

The document also mentions ongoing work in assessing the impact of artificial intelligence (AI) on UK markets and maintaining a pro-innovation and technology-agnostic approach.

Focus Areas

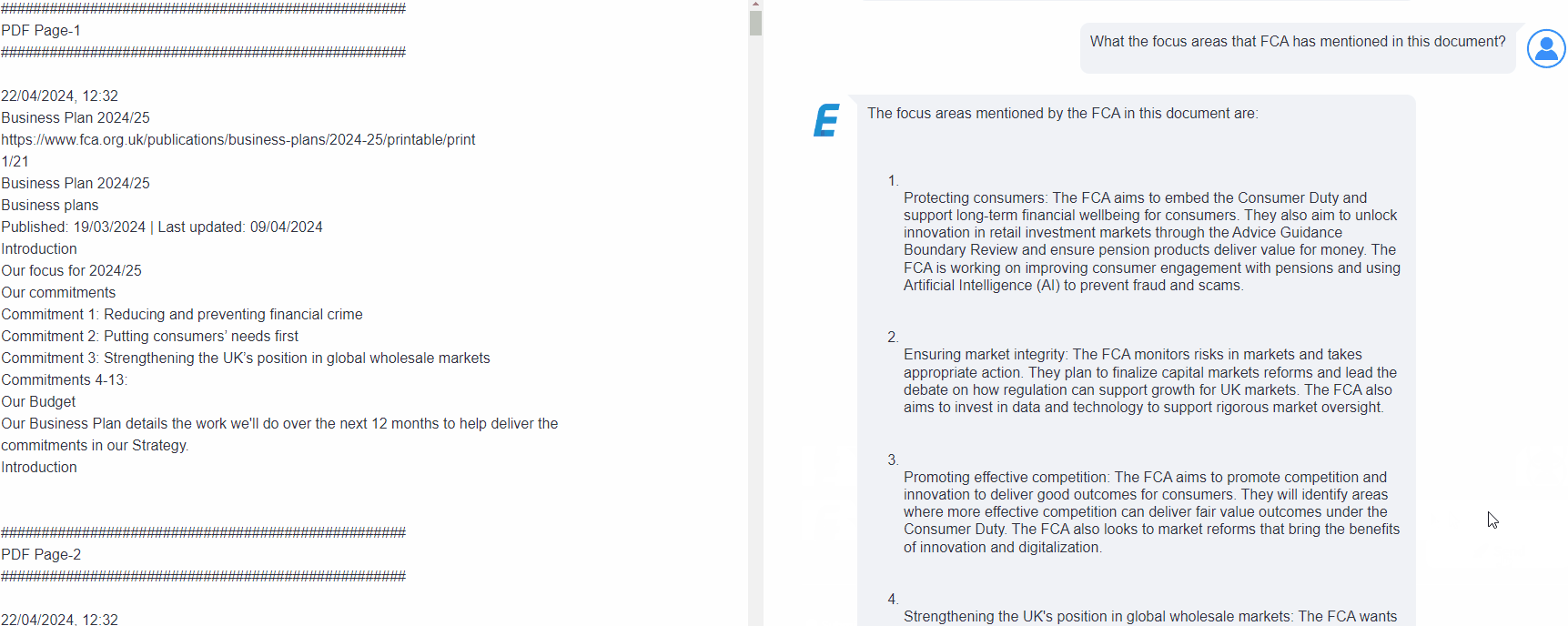

- Protecting consumers: To embed the Consumer Duty and support long-term financial wellbeing for consumers. To unlock innovation in retail investment markets through the Advice Guidance Boundary Review and ensure pension products deliver value for money. To work on improving consumer engagement with pensions and using Artificial Intelligence (AI) to prevent fraud and scams.

- Ensuring market integrity: To finalize capital markets reforms and lead the debate on how regulation can support growth for UK markets. To invest in data and technology to support rigorous market oversight.

- Promoting effective competition: To promote competition and innovation to deliver good outcomes for consumers. To identify areas where more effective competition can deliver fair value outcomes under the Consumer Duty. The FCA also looks to market reforms that bring the benefits of innovation and digitalization.

- Strengthening the UK’s position in global wholesale markets: To strengthen UK’s position in global wholesale markets and host markets that support the domestic economy and growth. To have a clear, well-understood, and trusted regulatory framework that supports fair value determination.

- Reducing and preventing financial crime: To increase their auto-detection capabilities of problem firms and individuals, quickly identify and cancel firms that do not meet Threshold Conditions and use regulatory tools to prevent harm to consumers and markets. To take assertive action on market abuse.

Key Commitments

Reducing and preventing Financial Crimes

- Take a data-led approach: To use data and intelligence to identify potential harm and take supervisory and/or enforcement action. This approach allows them to target higher risk firms and activities more effectively.

- Tackle scams and fraudulent websites: Take assertive action to tackle scams and fraudulent websites. This includes identifying and requesting platforms to remove unauthorized financial promotions, associated websites, and social media accounts.

- Collaboration with partners: To continue to work with partners, such as the National Economic Crime Centre (NECC), to support system-wide improvements and strengthen the overall response to financial crime.

- Proactive assessments of anti-money laundering systems and controls: Focus on proactive assessments of anti-money laundering systems and controls for firms deemed higher risk. This will help ensure that these firms have robust measures in place to prevent money laundering and the flow of illegitimate funds.

- Strengthen supervision of firms’ sanctions systems and controls: To strengthen its supervision of firms’ sanctions systems and controls. This will help ensure that firms have effective measures in place to comply with sanctions regulations and prevent financial crime.

Putting Consumers’ Needs First

- Ensure that firms act in good faith towards consumers and avoid causing them foreseeable harm. This means that firms should prioritize the well-being and best interests of consumers in their business practices.

- Ensure that consumers are sold products and services that meet their needs, characteristics, and objectives. Firms should consider the diverse needs of all consumers, including those with characteristics of vulnerability, and tailor their offerings accordingly.

- Ensure that consumers pay a fair price for products and services. Firms should ensure that the prices they charge represent fair value, and if any products or services are found to provide poor value, they should either be improved or removed from the market.

- Equip consumers with the right information to make informed decisions about their products and services. Firms should provide consumers with clear, accurate, and timely information that enables them to make effective decisions about their financial products and services.

- Ensure that consumers receive good customer service. Firms should prioritize providing high-quality customer service to consumers, addressing their queries and concerns promptly and effectively.

- Build consumer confidence in financial services markets. Firms should work towards creating an environment where consumers have trust and confidence in the financial services industry, knowing that their needs and interests are being prioritized.

- Encourage firms to innovate, supporting growth and driving effective competition in the interests of consumers. Firms should be encouraged to develop innovative products and services that meet the evolving needs of consumers, while also promoting healthy competition in the market.

Strengthening the UK’s position in global wholesale markets

- Encourage innovation and evolving markets: Support industry work on T+1 settlement, which aims to increase efficiency in the markets.

- Update the regulatory framework: To continue to update the regulatory framework to ensure it remains clear, well-understood, and trusted by all market participants. This includes delivering a set of Primary Market policy reforms, concluding the review of the Listing Regime, and publishing proposals for a new public offer and admission to trading regime.

- Consultation on regulatory changes: To consult on regulatory changes to introduce more options on how to pay for investment research. This is aimed at promoting transparency and fairness in the market.

- Ensuring venue resilience: To work on ensuring that venues are able to deal with and remain resilient in extreme events. This includes consulting on proposals for the commodity position limits regime, which aims to prevent excessive speculation and maintain market stability.

- Implementing derivative reporting rules: To ensure that derivative markets are ready to implement the new derivative reporting rules under the UK European Market Infrastructure Regulation (UK EMIR) in September. This is aimed at enhancing transparency and reducing systemic risk in the derivatives market.

Preparing financial services for the future

- Reducing and preventing serious harm: This involves implementing controls and processes to identify and mitigate risks that could lead to harm for consumers and the financial system. This includes monitoring and addressing issues such as fraud, misconduct, and unethical practices.

- Setting and testing higher standards: This priority focuses on establishing and enforcing regulations and standards that promote fair and transparent financial services. It involves conducting market studies and assessments to ensure that firms are meeting these standards and taking appropriate actions if they are not.

- Promoting competition and positive change: This priority aims to foster a competitive and innovative financial services sector that benefits consumers. It involves promoting fair competition, encouraging new entrants into the market, and supporting positive changes that enhance the efficiency and effectiveness of financial services.

- Facilitating international competitiveness and growth: This secondary objective focuses on aligning the UK financial services sector with international standards to ensure its competitiveness and long-term growth. It involves collaborating with international regulatory bodies and promoting the UK as an attractive destination for financial services.

Dealing with problem firms

- Increase auto-detection capabilities: To enhance its ability to proactively identify problem firms and individuals. This involves implementing advanced technologies and analytics to detect any potential issues or misconduct.

- Cancel firms that do not meet Threshold Conditions: To quickly identify and, if necessary, cancel the authorization of firms that fail to meet the Threshold Conditions. This ensures that only compliant and trustworthy firms operate within the financial industry.

- Use regulatory tools to prevent harm: To utilize a full range of regulatory tools to prevent harm to consumers and markets. This includes implementing and enforcing regulations, conducting inspections and audits, and taking appropriate enforcement actions against non-compliant firms.

- Identify barriers in the regulatory framework: To assess its regulatory framework to identify any barriers that may hinder its ability to take action against problem firms. This involves reviewing existing regulations, policies, and procedures to ensure they are effective and aligned with the institution’s objectives.

Taking assertive action on market abuse

- Increase the ability to detect and pursue cross-asset class market abuse: To enhance its capabilities in detecting and addressing market abuse across different asset classes. This includes utilizing advanced analytics such as network analysis and cross-asset class visualizations to improve market monitoring and intervention in Fixed Income and Commodities.

- Transfer MiFID data reporting regimes: As part of the Senior Managers and Certification Regime (SM&CR) process, to issue a discussion paper on transferring the MiFID data reporting regimes for transactions (RTS 22) and reference data (RTS 23). This transfer aims to ensure a proportionate market abuse regime for Crypto Assets and the PISCES facility.

- Extend data reporting supervision approach: To extend its data reporting supervision approach to European Market Infrastructure Regulation (EMIR), Securities Financing Transactions Regulation (SFTR), and Orderbook regimes. This extension will involve increasing resources and capabilities to influence international markets data strategy.

- Publish results of peer review: To publish the results of its peer review of market abuse systems and controls in providers of Direct Market Access. This review aims to assess the effectiveness of systems and controls in preventing market abuse and ensuring market integrity.

Reducing harm from firm failure

- Anticipating and identifying firms at risk of failure: To use data and horizon-scanning mechanisms to anticipate firms that are at risk of failure. To allow for early intervention and appropriate response to protect consumers and ensure market integrity.

- Effective management of severe market shocks: To develop strategies and measures to minimize the adverse impact of firm failure on consumers and markets.

- Sharing relevant information: To support the industry by sharing relevant information identified through data analysis, financial resilience return, and everyday work. This includes examples of good and poor practices of wind-down planning, which can help firms better prepare for potential failure and mitigate harm to consumers.

Environmental, Social and Governance (ESG) priorities

- Integration of Sustainability Disclosure Requirements and Investment Labels: To integrate these requirements and labels across the market. This includes implementing the anti-greenwashing rule and guidance. The FCA will continue to expand this regime, starting with the consultation on Portfolio Management in 2024.

- Engagement on new and emerging risks: To actively engage with UK and international partners to address new and emerging risks related to ESG. This includes working on Transition Finance and preparing to have regard to a ‘Nature’ regulatory principle coming into force.

Shaping digital markets to achieve good outcomes

- To collaborate closely with the Digital Markets Unit in the Competition and Markets Authority on the new pro-competition regime for digital markets.

- To drive greater cooperation on digital issues through the Digital Regulation Co-operation Forum, which includes piloting an AI & Digital Hub to support innovators.

- To robustly investigate digital consumer journeys and firms using sludge practices. To closely monitor and investigate any practices that may mislead or harm consumers in the digital space.

- To ensure that digital markets are fair, transparent, and beneficial for consumers and markets, while also recognizing the risks and opportunities associated with digital innovation.

Improving the redress framework

- Redress Guidance for Firms: To continue its work on providing guidance for firms regarding redress. This guidance aims to ensure that consumers receive appropriate and efficient redress when things go wrong.

- Complaints Reporting: To continue its work on complaints reporting. This involves monitoring and analyzing complaints made by consumers and taking appropriate actions to address any issues identified.

- Advice Guidance Boundary Review: To conduct a review of the advice guidance boundary. This review aims to ensure that firms understand and meet the FCA’s expectations regarding the provision of advice to consumers.

- Capital Deduction for Redress: To propose a capital deduction for redress for personal investment firms. This measure aims to ensure that firms that cause harm bear more of the cost of redress.

- Review of Lead Generation in the CMC Sector: To review lead generation in the Claims Management Companies (CMC) sector. This review aims to assess the practices and effectiveness of lead generation in this sector.

- Historic Discretionary Commission Arrangements in the Motor Finance Market: To continue its work on historic discretionary commission arrangements in the motor finance market. This work involves analyzing the issues and considering the legal steps that may be necessary to address any concerns.

- Collaboration with Financial Ombudsman Service and Financial Services Compensation Scheme: To work with the Financial Ombudsman Service and the Financial Services Compensation Scheme to ensure open working practices on areas they share. This collaboration aims to enhance the effectiveness of redress processes and improve outcomes for consumers.

Enabling consumers to help themselves

- Robust assessments of firms’ applications to approve financial promotions for unauthorised firms: To continue to assess and scrutinize firms’ applications to approve financial promotions. This ensures that only authorized firms with the necessary permissions are allowed to promote financial products and services. By including information about firms’ permissions to approve promotions in their Register, consumers can easily access this information and make informed decisions.

- Acting quickly against non-compliant financial promotions: To use new sources of data to identify and take swift action against authorized firms that approve and issue non-compliant financial promotions. This proactive approach aims to prevent mis-selling and financial losses for consumers.

Minimising the impact of operational disruptions

- Ensuring firms meet operational resilience standards: To continue to deal with firms that cannot meet their standards on operational resilience. By March 31, 2025, all relevant firms will be required to maintain their important business services without causing intolerable harm to consumers and markets.

- Clarifying expectations on reporting operational incidents: To publish a consultation paper that will clarify their expectations on how firms should report operational incidents to them. This will help ensure that both the FCA and firms are able to respond effectively to minimize harm to consumers and markets.

- Addressing systemic risk from critical third parties: To publish a Consultation Paper that proposes new rules to address the systemic risk that critical third parties present to the financial sector. This indicates that the FCA recognizes the increasing levels of systemic risk build-up in the system due to reliance on these critical third parties.

Improving oversight of Appointed Representatives

- Targeting resources through deeper analysis of existing data: To analyze existing data to identify areas where principals may not be adequately overseeing their Appointed Representatives (ARs). This analysis will help prioritize resources and focus on areas of higher risk.

- Using significantly improved data: To utilize updated Gateway forms, new regulatory returns, and a dataset covering all ARs to gather more comprehensive and accurate information. This improved data will enable better oversight and monitoring of AR activities.

- Strengthening scrutiny and engagement with principal firms: To enhance its scrutiny and engagement with principal firms during the process of appointing ARs. This will involve closer monitoring and assessment of the firms’ oversight practices to ensure compliance with regulations.

- Assertive supervision of high-risk principals: To employ its regulatory tools and appropriate enforcement actions to supervise high-risk principals more assertively. This will help mitigate the risks associated with misconduct by ARs and ensure market integrity.